Today’s market analysis on behalf of Michael Brown Senior Research Strategist at Pepperstone

3rd February 2025

DIGEST – Stocks have slumped and the dollar rallied to start the new trading week, as Trump’s weekend tariff announcements are digested, ahead of this week’s busy slate of event risk.

WHERE WE STAND – Well, here we go then, we’re off and running with perhaps the most stupid trade war ever.

After some ‘will he or won’t he’ sources reporting into the close on Friday, it turned out that, in fact, he would. Of course, I’m alluding here to President Trump imposing 25% tariffs on US imports from Canada and Mexico (10% on Canadian energy), as well as an additional 10% levy on goods coming from China.

Predictably, this has been met with a tit-for-tat response; Canada will impose 25% tariffs on 155bln CAD of US goods, Mexico’s economy minister is set to implement reciprocal tariffs on the US, while China has also vowed to put in place counteractive measures as well as filing lawsuits against the tariff imposition.

Perhaps equally as predictably, financial markets have digested the tariff news poorly, having failed to adequately price such a scenario before the weekend. The dollar, naturally, opened firmer against all G10 peers, with the EUR notably underperforming – besides the obvious CAD weakness, with the loonie at over 2-decade lows – presumably amid concerns that the EU may well be the next to have tariffs imposed. Equity futures, meanwhile, have lurched lower across the globe, with front S&P futures down around 2% at the time of writing, while the Treasury curve has twist flattened, as the front-end prices upside inflation risks, and the long-end finds haven demand.

So, where does this all leave us?

From a political perspective, we’re in pretty much the same place. Tariffs continue to be used as a negotiating tool, for President Trump to force through his political priorities. Ostensibly, this is to reduce trade deficits, and the supply of fentanyl into the US. In reality, this agenda is more about renegotiating the USMCA trade deal early, as well as re-shoring key industries into the US, in an attempt to juice the economy, and further the ‘America First’ campaign rhetoric.

From a macro perspective, the imposition of tariffs raises upside inflation, and downside growth risks. In turn, this heightens the chances that the FOMC will stay on pause for longer, pushing back the timing of cuts to the fed funds rate towards the end of H1 at the soonest. Furthermore, the increased uncertainty now introduced to the outlook makes the December SEP somewhat redundant, while also making the March SEP tougher to predict, as the impact of tariffs is unlikely to be clear by then. In any case, slapping tariffs on your two closest neighbours isn’t a particularly sound macroeconomic or fiscal policy stance.

From a market perspective, there are a few considerations.

Firstly, an elevated degree of policy uncertainty persists, and is likely to ratchet higher in coming days, as tit-for-tat tariff impositions have the potential to escalate further. This, in turn, should lead to a considerably higher degree of cross-asset volatility, as market participants continue to have great difficulty in accurately discounting the future policy path, which probably doesn’t exist in any sort of concrete way.

Secondly, the USD should continue to strengthen, by default if nothing else, as the impact of tariffs becomes clear. The reasonable assumption is that, while tariffs benefit nobody, they are likely to harm the US economy the least, by extension leading to a continuation of the long-running ‘US exceptionalism’ theme, and leaving the greenback as the cleanest dirty shirt in the laundry once again.

Thirdly, barring a significant hit to economic growth, and some near-term choppiness, the path of least resistance for equities should continue to lead to the upside. Earnings growth, thus far, remains solid, with consumer spending having also proved resilient in recent months, with potential re-shoring likely also to boost some sectors in the market which continue to play catch-up to the ‘Magnificent Seven’. Trump, also, seems to view equity performance as a barometer of his own success, and hence has some degree of an incentive not to go too far on tariffs, and take a wrecking ball to the bull market.

Lastly, higher vol, and elevated policy uncertainty, should see demand for havens remain healthy. Treasuries, given upside inflation risks, are probably not the best place to hide out here, while the FX space will continue to be roiled by trade headlines, likely leading most participants towards gold. The yellow metal trades at fresh record highs in the spot market, and momentum looks likely to remain with the bulls for the time being.

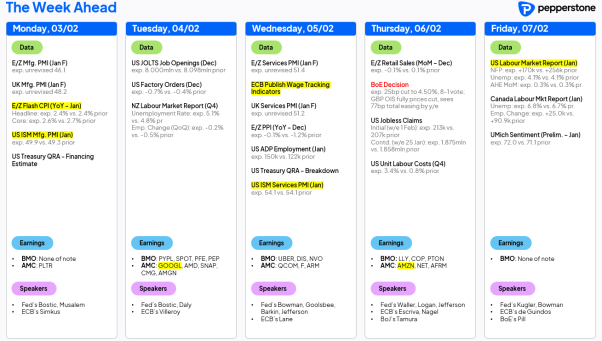

LOOK AHEAD – Besides tariffs, the week ahead presents plenty for participants to get their teeth into, as the calendar graphic evidences.

On the data front, Friday’s US labour market report is the obvious highlight, though I’d argue risks to the +170k NFP consensus figure tilt to the downside, owing to the impact of wildfires in California. Elsewhere, the latest US ISM manufacturing and services PMIs will also be closely watched, as will the latest eurozone inflation and earnings data, even if neither should derail the ECB from another 25bp cut in March.

Meanwhile, ‘Mag 7’ earnings continue, with Alphabet (GOOGL) and Amazon (AMZN) set to report, as participants continue to price two-sided risks around the AI theme, and are in an unforgiving mood in terms of earnings misses after the emergence of DeepSeek AI in recent weeks, and the threat that it may pose to the US ‘big tech’ names.

Lastly, the Treasury announce quarterly refunding estimates on Monday, and the breakdown of borrowing on Wednesday, providing something else for Treasury participants to grapple with, along with the impacts of the aforementioned tariffs.