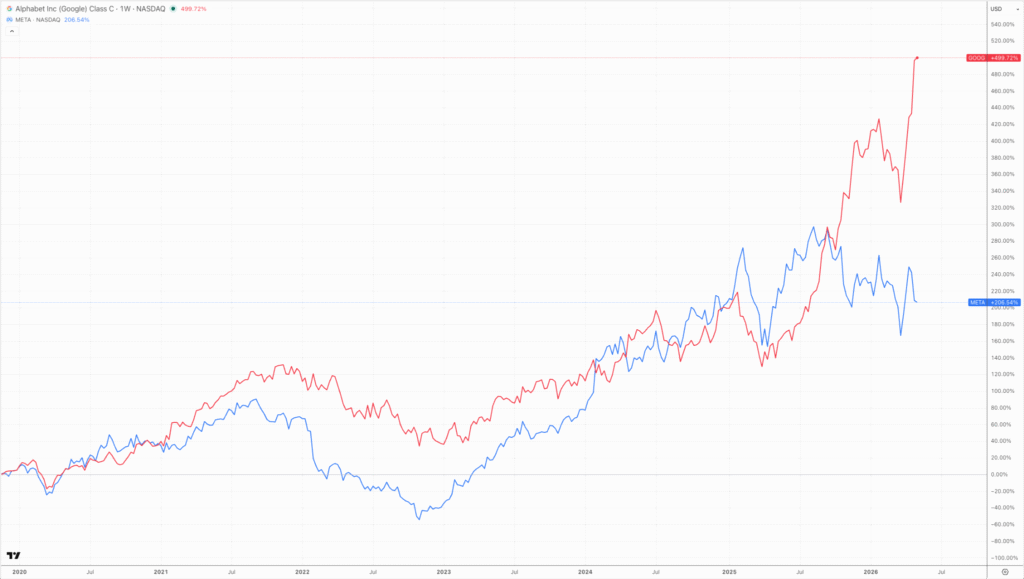

The multidirectional movement of Alphabet and Meta shares after the publication of quarterly reports has become one of the clearest signals of the current reassessment phase in the technology sector. Alphabet’s capitalization growth of more than 10%, against the backdrop of a 10% decline in Meta shares, reflects less a reaction to operating results and more an emerging market differentiation between artificial intelligence monetization models and companies’ ability to convert capital spending into sustainable cash flow.

In Alphabet’s case, the key driver was the Google Cloud segment, which recorded revenue growth of 63% year-on-year due to accelerated demand for enterprise AI solutions. In effect, the company is demonstrating a direct conversion of infrastructure investments into commercially measurable results. Artificial intelligence is being integrated into the existing cloud model and is enhancing its monetization potential rather than requiring a radical restructuring. Against this backdrop, the increase in projected capital expenditures to $180-190 billion is perceived by the market not as a risk, but as a reflection of already confirmed demand. Formally, this reinforces a model in which AI investments are offset by the scaling of the cloud business, partially mirroring the expectations surrounding the OpenAI IPO.

A completely different dynamic is observed at Meta, where record profits of $26.8 billion and revenue growth of 33% year-on-year failed to compensate for structural concerns regarding the quality of future investment returns. Despite the strong financial performance, the market focused on the increase in capital expenditures to $125-145 billion and the lack of a clear payback trajectory outside the advertising business. Additional pressure came from a decline in daily active users and growing regulatory and legal risks, including lawsuits about the impact of the company’s services on users’ mental health.

Meta demonstrates a model in which a significant portion of current profits is redistributed in favor of future AI infrastructure without a guarantee of its direct monetization. Unlike Alphabet, the company lacks a comparable cloud segment capable of absorbing these investments and converting them into sustainable external cash flow. This creates a structural gap between investment levels and potential returns, reflected in the more negative stock reaction visible on the heatmap.

Further pressure stems from the internal transformation of Meta’s business model. The effective abandonment of the metaverse as a priority did not reduce the cost burden. The accumulated losses of Reality Labs, exceeding $80 billion over several years, are now being replaced by an even more capital-intensive cycle of AI investments. At the same time, the company recognizes that its computing resource requirements continue to be systematically underestimated, while projections for the period beyond 2027 remain uncertain. This creates a situation in which the scale of expenses is growing faster than the company’s ability to quantify potential returns.

Structurally, the difference between the two companies is reflected in the mechanics of investment capitalization. Alphabet is converting AI demand into cloud revenue growth, forming a closed cycle between investment and monetization. Meta, by contrast, is redirecting cash flow from its high-margin advertising business into long-term infrastructure projects whose effectiveness remains unclear. As a result, the market is assigning a higher discount to Meta’s future earnings compared to Alphabet, despite the comparable scale of investments.

The market is no longer evaluating technology companies solely on revenue or profit growth, shifting the focus toward the ability of infrastructure spending to generate autonomous sources of capital return. This explains why even strong Meta reporting does not compensate for the lack of a transparent AI monetization model, while Alphabet receives a premium for the already functioning mechanism of converting capital expenditures into cloud revenue.

Collectively, the current dynamics reflect the emergence of a new investment division within the technology sector: between companies using AI to enhance an existing business model and companies attempting to build a new infrastructure paradigm around it. It is this gap, rather than absolute financial indicators, that is increasingly becoming a key driver behind the reassessment of the value of technology giants at the current stage of the cycle.