You shouldn’t lose 7.75 percent of every 403(b) contribution to hidden fees—that’s what one Florida teacher saw when $1,125 from her May paycheck dropped by $87.23. This guide keeps that from happening.

Florida offers a solid pension, yet its 403(b) marketplace is a maze of annuity pitches and conflicting advice. National best-of lists ignore those quirks, so we rated the seven vendors serving Florida in 2026 on cost, fund quality, fiduciary duty, service, and compliance.

Read on to learn which providers merit your paycheck deductions and how to spot fees before they drain tomorrow’s pension supplement.

How we picked the winners

We built a scorecard that treats your money like our own before naming any provider the best.

Cost came first. Because fees touch every paycheck, total participant cost carried a 30-point weight. Any provider that buried expenses in fine print dropped quickly.

Signature Financial Solutions’ review of a recent Government Accountability Office study reports that 403(b) investment fees stretch from just 0.01 percent to a punishing 2.37 percent—nearly a 240-fold spread.

On a $50,000 balance, the upper end can siphon more than $1,000 every single year, so weighting cost above every other factor simply protects teachers’ paychecks.

Investments were next. A lineup filled with low-cost index funds and target-date choices earned up to 20 points, while annuity-only menus lagged.

Fiduciary duty and transparency followed. Vendors that prove in writing that they put your interests first collected another 20 points. The 2022 SEC action against Equitable for misleading fee statements underscores why this factor matters.

Participant support mattered too. Florida’s districts sprawl, so we set aside 15 points for web tools, local reps, and clear education resources.

Reputation closed the list. Clean compliance records and a strong Florida track record added the final 15 points.

Each vendor started at zero. We scored them one to five on every factor, applied the weights, and totaled a crisp score out of 100. When two vendors tied, Florida-specific edges such as DROP rollover know-how or an in-state office broke the tie.

The ranking you see comes from math, public filings, and real-world experience, not marketing copy.

Florida’s 403(b) landscape in 2026: what’s shaping your choices

Florida is a retirement-planning paradox. We pay no state income tax and many public employees receive a solid pension, yet the 403(b) marketplace stays crowded with high-cost annuities and confusing vendor lists. Understanding the forces behind that tension helps you focus on providers that move the needle.

The first force is federal law. Secure Act 2.0 triggered automatic enrollment for new 403(b) plans in 2025. The same statute sought to permit lower-cost collective investment trusts (CITs), but securities rules are still pending. CITs function like mutual funds at a lower price, so forward-looking vendors are lining up to add them. If your district creates a plan, expect opt-out enrollment instead of an opt-in form.

Closer to home, the Florida Retirement System anchors many careers, but newer hires lean more on supplemental savings. That shift turns a 403(b) from a convenience to a necessity, especially for staff who leave before vesting or who plan to roll a DROP lump sum.

Regulators are adding pressure. After multimillion-dollar settlements over hidden fees, watchdogs now grade vendors on disclosure and advisor pay. Some legacy insurers already trimmed wrap fees and introduced index funds to keep district contracts.

Competition is also growing. Empower bought MassMutual and Prudential’s retirement units, while fintech platforms such as Aspire and Human Interest pitch streamlined plans for small nonprofits. Choice is broader, yet not every option meets our scorecard, which is why we narrowed the field to seven.

In short, Secure Act mandates, FRS dynamics, regulatory scrutiny, and new market entrants are reshaping the playing field. The seven providers you will see next are adapting the fastest.

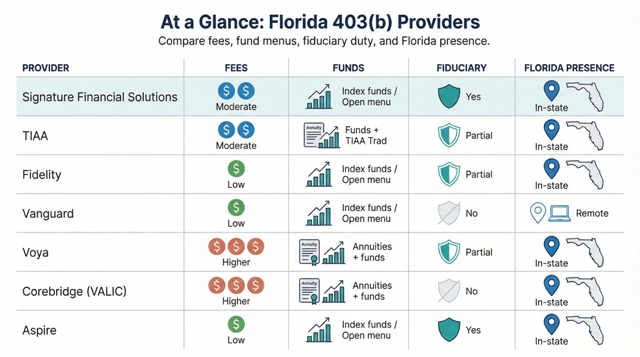

At a glance

You may not have time to read every mini-review, so use this cheat sheet for the four questions Florida staff ask first — fees, funds, fiduciary status, and local presence.

| Provider | Typical all-in cost | Investment menu highlights | Fiduciary to participants? | In-state footprint |

| Signature Financial Solutions | About 1.2 percent (0.20 fund ER, 1.0 advisory) | Open architecture using Vanguard, Fidelity, T. Rowe | Yes, fee-based fiduciary | Headquartered in Tampa |

| TIAA | Roughly 0.70 percent | TIAA Traditional plus broad mutual funds | Plan-level 3(21); not always personal | Campus reps statewide |

| Fidelity | 0.03 – 0.60 percent | Index funds, target dates, brokerage window | Optional 3(38) add-on | Investor Centers in Miami, Tampa, and more |

| Vanguard | 0.10 – 0.25 percent | Core index funds; no annuities | Product-only, no advice | Remote service via TPAs |

| Voya | 0.60 – 1.50 percent | Variable annuities and fund platform | Varies; many reps work on commission | Regional hub in Orlando |

| Corebridge (VALIC) | 1.0 – 2.0 percent | Fixed and variable annuities, funds | No, commission model | Teams in Miami-Dade and Tampa |

| Aspire | 0.30 – 0.45 percent | Twenty-five-thousand-plus funds through brokerage | Yes, 3(16) and 3(38) options | Headquarters in Tampa |

Three patterns stand out. First, pure mutual-fund platforms such as Vanguard, Fidelity, and Aspire cluster at the low-fee end, while insurance giants lean higher. Second, fiduciary alignment is not automatic; only three vendors extend it to every participant. Finally, a local office can be a tiebreaker when costs and menus look similar.

1. Signature Financial Solutions: the local fiduciary with skin in the game

We start with a firm that sells advice, not products. Signature Financial Solutions is a fee-based advisory firm in Tampa. While its team can earn commissions on insurance, they serve as fiduciaries, so their revenue rises only when your account grows. That transparency, rare in K-12 vendor lists, secured the top score on our chart.

Signature Financial Solutions employer retirement plans webpage screenshot

Cost comes first. SFS charges about one percent of assets for ongoing guidance and steers plans toward institutional-share mutual funds that average 0.20 percent. All-in, a Florida teacher lands near 1.2 percent per year, which is less than half the state’s annuity-heavy norm. Every fee appears in writing; none hide in surrender charges or rider add-ons.

That vigilance pays off. A Government Accountability Office analysis shows 403(b) fees ranging from 0.01 percent to 2.37 percent; over a 30-year career the difference can top six figures.

Signature unpacks those numbers in its plain-English guide to maximizing a 403B Account and outlines simple moves, such as shifting to institutional-share index funds, that slash costs without sacrificing growth.

Independence is the bigger story. SFS builds open-architecture menus, so your district can pair Vanguard index funds, T. Rowe Price active options, and even a brokerage window for power users. The firm signs on as a 3(38) fiduciary, taking legal responsibility for fund selection and monitoring. That move shifts a share of regulatory risk away from the plan sponsor.

On campus, advisors run lunch-and-learns on FRS integration, DROP timing, and Secure 2.0 catch-ups. Teachers leave knowing how a 403(b) fits with their pension, not just which form to sign.

The lone drawback is brand recognition. SFS lacks a national name, and districts still need a record-keeper such as Fidelity or Aspire to hold assets. Yet for committees seeking unbiased guidance and a single point of accountability, Signature Financial Solutions remains the front-runner.

2. TIAA: built for lifelong educators who crave predictable income

TIAA has helped faculty for more than one hundred years, and the track record shows. For Florida universities and large nonprofits, the company offers a one-stop 403(b) package that combines mutual funds with TIAA Traditional, a fixed-rate account that converts to lifetime paychecks in retirement.

TIAA retirement services homepage screenshot for Florida educators

That predictable income steadies investors during market swings. Participants holding TIAA Traditional receive a declared interest rate each year, with no quarterly resets. Many veteran professors view it as a personal pension on top of FRS.

Fees sit near the middle of our list, at about 0.30 percent for administration plus fund expenses of roughly 0.40 percent. While not the lowest, the price is competitive for institutional-class shares and the built-in guarantee. Over the past two years, several Florida college plans negotiated additional rebates that trimmed costs as assets grew.

Service is another strength. TIAA staffs campus offices in Tampa, Gainesville, and Jacksonville, so employees can talk through rollover timing or Roth conversions in person. Online calculators model Secure 2.0 catch-up limits and show how a lump-sum DROP payout could annuitize inside the plan.

Two cautions remain. The annuity rules can feel dense, and TIAA reps serve as educators, not personal fiduciaries. If you prefer self-directed index funds only, pairing TIAA with a second vendor such as Fidelity can broaden your menu. Still, for career educators who want stability and hands-on help, TIAA earns the silver spot.

3. Fidelity Investments: low-cost menus plus a walk-in help desk

Fidelity blends two strengths that few rivals combine: rock-bottom index funds and brick-and-mortar service centers. For Florida educators who want a cheap core lineup and a human to answer “Should I go Roth?” at lunch, that mix delivers.

Start with price. Many midsize districts negotiate Fidelity’s record-keeping fee to zero once assets cross a modest threshold. From there, flagship index funds cost as little as 0.02 percent. Even without fee waivers, total expenses stay well below one percent, far less than typical annuity contracts.

Choice is the second win. Employees can keep it simple with Freedom target-date funds or open a Self-Directed Brokerage to buy nearly any ETF on the market. That breadth satisfies the teacher who wants to “set it and forget it,” as well as the tech coach who insists on owning an ESG fund or Treasury ETF the core lineup lacks.

Service completes the package. Fidelity staffs Investor Centers in Miami, Tampa, Orlando, and Jacksonville. Walk in with a statement, and you leave with a printed asset-allocation proposal at no extra cost and without an annuity pitch. Phone reps answer questions until 10 pm Eastern, which helps night-owl graders.

There are limits. Fidelity is a record-keeper first, not a fiduciary advisor. Committees that want a third party to pick and monitor funds must add an outside 3(38) or handle that role internally. For the smallest nonprofits, those with under one million dollars in plan assets, setup fees can feel steep next to fintech entrants such as Aspire.

For most Florida schools and charities seeking a big-brand provider that respects budgets and empowers DIY investors, Fidelity takes the bronze.

4. Vanguard: squeeze every penny out of each paycheck

If your mantra is “fees matter most,” Vanguard tops the vendor list. The firm’s co-op structure returns profits to fund holders, so expense ratios stay razor thin. In a Florida 403(b), that means a flat five-dollar monthly record-keeping charge (sixty dollars a year) and fund costs near 0.10 percent. Independent comparisons of 403(b) pricing confirm those figures. A teacher who saves five hundred dollars a month for thirty years keeps about forty thousand dollars more than someone in a two-percent annuity. Vanguard’s Total Stock Market Index offers broad diversification for three basis points, cheaper than many institutional shares elsewhere.

Simplicity is the next draw. The core menu sticks to broad index funds, target dates, and nothing more. There are no bonus riders, surrender periods, or multi-tiered annuity crediting rates to untangle. You pick a fund, set payroll deductions, and get back to lesson planning.

The trade-off is service style. Vanguard runs lean, so support is phone and web only. Districts that want on-site reps or glossy enrollment fairs may see that as a gap. Some K-12 plans also cannot contract with Vanguard directly; they access the funds through a TPA such as Aspire, which adds a small custody fee.

Even with those hurdles, Vanguard stays the purest option for educators who trust low-cost indexing and prefer do-it-yourself allocations. If that sounds like you, ask your benefits office to add Vanguard or a Vanguard-powered open-architecture chassis. Your future self will thank you at the retirement party.

5. Voya Financial: flexible plan design with a human touch

Voya sits between mutual-fund purists and insurance stalwarts. The company built its name on annuities, yet its modern 403(b) platform lets Florida districts decide how much insurance they really want. One campus might turn off annuities entirely and run a low-cost mutual-fund lineup, while another keeps a stable-value option for staff who worry about volatility.

Pricing reflects that mix. Administrative wraps usually fall between 0.60 and 1.50 percent, with fund expenses on top. In 2024 Voya introduced a fee-transparency dashboard that breaks costs into clear buckets — record-keeping, investments, and advisor pay — so committees can trim fat before contracts renew.

Service is Voya’s calling card. Regional teams in Orlando handle payroll files, loan processing, and on-site enrollment meetings. Teachers in Pinellas, Broward, and nearby counties praise quick turnaround on hardship withdrawals, a weakness for slower vendors. The company also funds financial-wellness workshops that include personalized video recaps employees can replay later.

Watch the reps, though. Many work on commission, so fiduciary alignment depends on the individual advisor rather than the corporate logo. For small nonprofits, Voya’s asset-based admin fee can sting until the plan grows.

Choose Voya when you value hands-on support and need the freedom to tailor investments, but walk in with a clear fee benchmark and a sharp pencil.

6. Corebridge Financial (AIG / VALIC): annuity horsepower with six decades of Florida experience

Corebridge, the rebranded retirement arm of AIG, has served Miami-Dade teachers since 1964. That longevity gives the company deep knowledge of FRS payroll quirks, DROP rollovers, and district bargaining cycles. For employees who want principal guarantees, its fixed annuity still offers one of the highest floor rates in the market.

The past, however, includes a caution. In 2020 the SEC fined the firm forty million dollars for secretly paying a teachers’ union entity to secure product endorsements and then capped certain advisor fees. Corebridge has since improved disclosures and trimmed asset-based charges for new Florida contracts, but sponsors should review every line.

Cost today averages about one percent for the annuity wrapper, plus between 0.50 and 1.00 percent in fund expenses. That price is higher than Vanguard yet lower than many legacy variable-annuity vendors once surrender periods end. Districts can also negotiate a mutual-fund-only sleeve that skips the annuity mortality and expense fee.

Service remains the bright spot. Dedicated Corebridge teams sit in Tampa, Miami, and other hubs, handle onsite counseling, and run evening webinars on laddering annuity buckets with DROP payouts. Participants praise quick loan processing and straightforward e-sign tools introduced in 2023.

Corebridge fits when your workforce values insurance guarantees and wants a vendor fluent in district procedures. Insist on the post-2020 fee schedule and consider pairing Corebridge with a low-cost mutual-fund provider so employees can choose between safety and growth without leaving the plan.

7. Aspire (PCS Retirement): open-architecture fintech that lets you build your own menu

Aspire closes our list as the value play hiding in plain sight on many district vendor grids. Think of it as the Vanguard of record-keepers, designed to stay out of your way and keep fees transparent.

Aspire PCS Retirement open-architecture 403b platform screenshot

Costs are blunt and simple. Each account pays a forty-dollar annual charge plus 0.15 percent of assets for custody. Everything else depends on the funds you choose. Pick Vanguard or Fidelity index funds and your total expense can stay below 0.30 percent, a rate rare in K-12 plans long filled with two-percent annuities.

Flexibility is the main draw. Aspire’s brokerage window opens access to more than 25,000 mutual funds, ETFs, and even DFA institutional shares. A novice teacher can park cash in a target-date fund while the district’s finance instructor builds a factor-tilted portfolio, all under one roof.

Governance is solid as well. Aspire can serve as both 3(16) administrative fiduciary and 3(38) investment fiduciary, lifting compliance work off small nonprofits. Its Tampa headquarters adds local support and a tech stack that rivals larger national providers.

Guidance is the trade-off. Aspire supplies the platform; advice is optional and usually comes from an outside RIA that may charge an additional fee. Districts should decide whether they want a bundled advisor or will rely on internal education.

If your goal is maximum choice at minimum cost, and you are comfortable steering your own allocation or pairing with a third-party fiduciary, Aspire is the low-fee runway you have been looking for.

Honorable mentions: solid backups that sit just outside the top seven

Several well-known names missed our main list. Each offers real strengths, yet one or two friction points kept them out of medal range. Use them as fee benchmarks or niche add-ons when your workforce needs a specific feature.

Equitable. Local agents are available, and the investment lineup is broad, but the firm’s 2022 SEC fine over misleading fee statements still weighs on trust. Treat Equitable as a comparison quote rather than a first pick until it posts a multi-year record of transparency.

Lincoln Financial. Strong financial-strength ratings and a polished managed-account program make Lincoln popular with hospital systems that want customized advice. Costs, however, tend to hover above one percent for smaller plans, and the fund menu leans on proprietary options.

Security Benefit. The NEA Valuebuilder brand and the low-cost DirectInvest window draw teachers in, yet most participants default into higher-fee annuity contracts while DirectInvest sits three clicks deep. Unless a district can force that window to the front page, savings often fail to appear.

Empower. After buying MassMutual and Prudential’s retirement units, Empower now runs a slick participant portal and commands massive scale. In Florida K-12, though, it is still the new kid on the block, with limited field staff and few district references. Give it time; in a year or two it may crack the main list.

Conclusion

Bottom line: these providers can work, but only when a committee negotiates hard on fees and demands fiduciary alignment. If they sharpen pricing and improve disclosure, they could join the core rankings in our next update.