Every year, Indian households move staggering sums across borders: tuition fees for children studying in the US and Canada, support for family members working in the Gulf, investments in foreign equities, and payments for international business. The World Bank consistently ranks India as the world’s largest recipient of remittances — but the flow runs both ways, and the timing of every outbound transfer hangs on a single, volatile number: the USD/INR exchange rate.

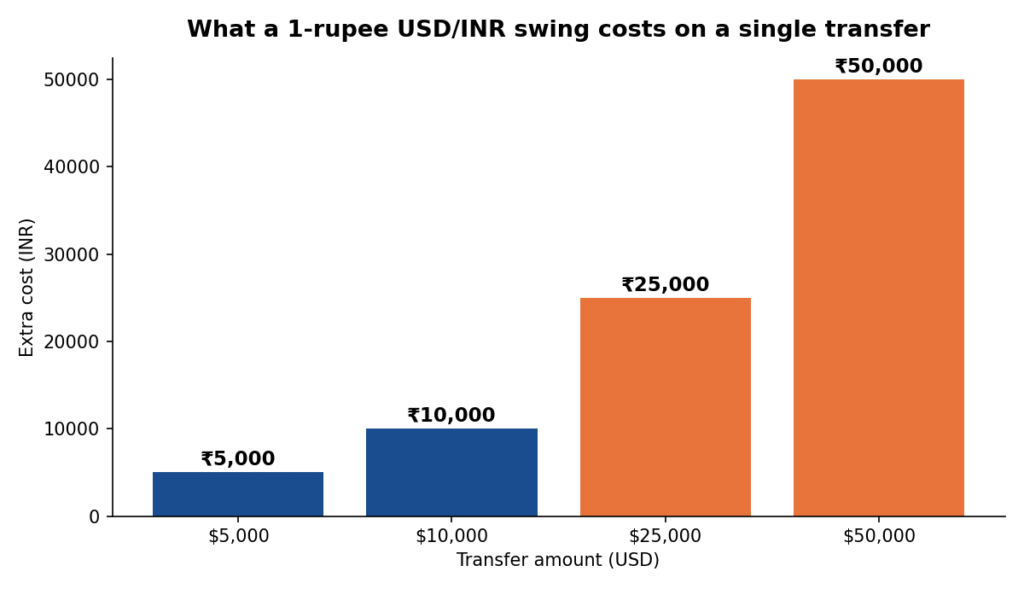

A swing of one rupee per dollar on a $25,000 university tuition payment is a difference of 25,000 rupees — roughly a month’s rent in many Indian cities. Yet most families still convert money the same way they did twenty years ago: when the deadline arrives, at whatever rate the bank offers that morning.

A growing number of Indian retail investors and self-directed savers are changing that habit. Here is what they are doing differently.

Treating the transfer date as a window, not a deadline

The first shift is mental. A tuition payment due on August 1 does not have to be converted on August 1. It can be converted any time in the preceding weeks — whenever the rate is favourable — and parked in the destination currency.

That turns a one-day gamble into a multi-week decision window, and it is exactly the situation where forecasting tools earn their keep. Modern analytics platforms publish algorithmic projections for major pairs; checking an independent USD to INR forecast before choosing a conversion date gives a family a data-grounded view of where the pair is likely to trade over the coming days and weeks — including the projected range, not just a single headline number.

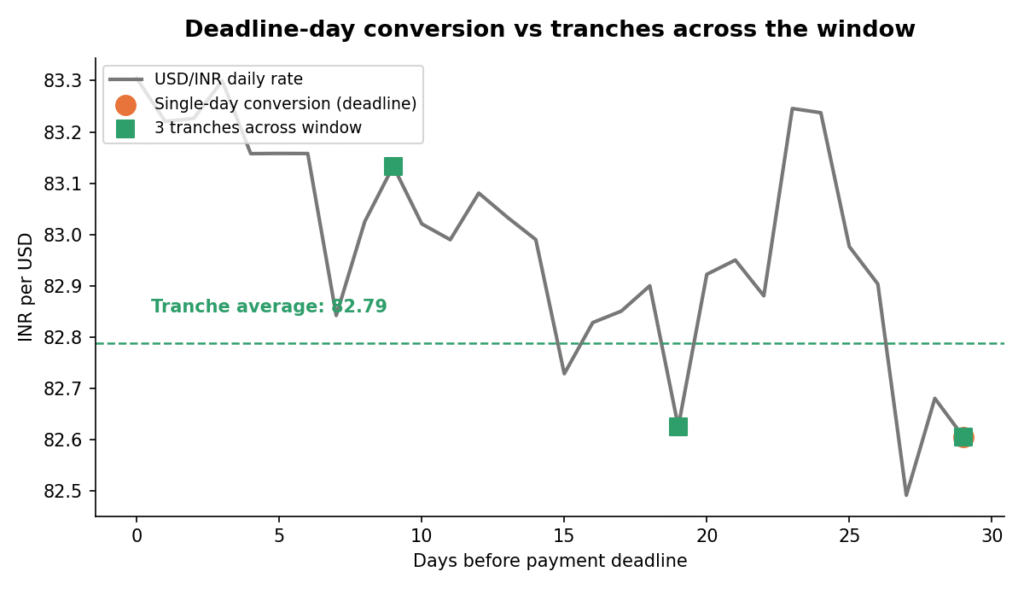

The range matters more than the midpoint. If the projection shows a narrow band, waiting carries little risk either way. If the band is wide — typically around major central bank meetings or inflation prints — splitting the conversion into two or three tranches spreads the risk the same way systematic investment plans (SIPs) spread equity risk.

What a one-rupee swing costs

Borrowing the SIP mindset for currency decisions

Indian investors already understand rupee-cost averaging better than almost any retail population in the world — SIPs in mutual funds have made it a household concept. The same logic applies directly to planned foreign-currency expenses.

Instead of converting 100% of a known future expense at one moment, disciplined households convert fixed slices at regular intervals across the available window. The arithmetic is identical to a SIP: more dollars are bought when the rupee is strong, fewer when it is weak, and the average rate lands comfortably away from the worst case. No prediction required — though a forecast helps decide when to begin.

Tranches vs deadline-day conversion

Checking the macro calendar before trusting any projection

The experienced minority adds one more step: before acting on any forecast, they check what scheduled events fall inside its window. A US Federal Reserve decision, an RBI policy announcement, US CPI data — these are published months in advance and reliably widen currency ranges. The Reserve Bank of India publishes its full meeting calendar on rbi.org.in, and no currency projection that straddles one of those dates deserves full confidence.

This habit — pairing a model’s output with the public events calendar — is what separates informed timing from coin-flipping. A forecast is a probability distribution, not a promise; scheduled macro events are the moments when that distribution stretches.

What the data-driven platforms actually offer

The new generation of forecasting services differs from old-style bank research notes in three practical ways. First, coverage: platforms such as Becoin, which publishes model-driven projections across currencies, stocks, and digital assets in more than forty languages, update forecasts continuously rather than quarterly. Second, transparency: the better services display how accurate their past projections proved at each horizon, letting users calibrate how much weight to give the next one. Third, accessibility: the projections are free to check, which matters for a family making two or three transfers a year, not two or three a day.

None of this turns a household into a trading desk — and it should not. The goal is narrower and more achievable: avoid converting a large sum on a visibly bad day, and stop treating exchange rates as unknowable weather.

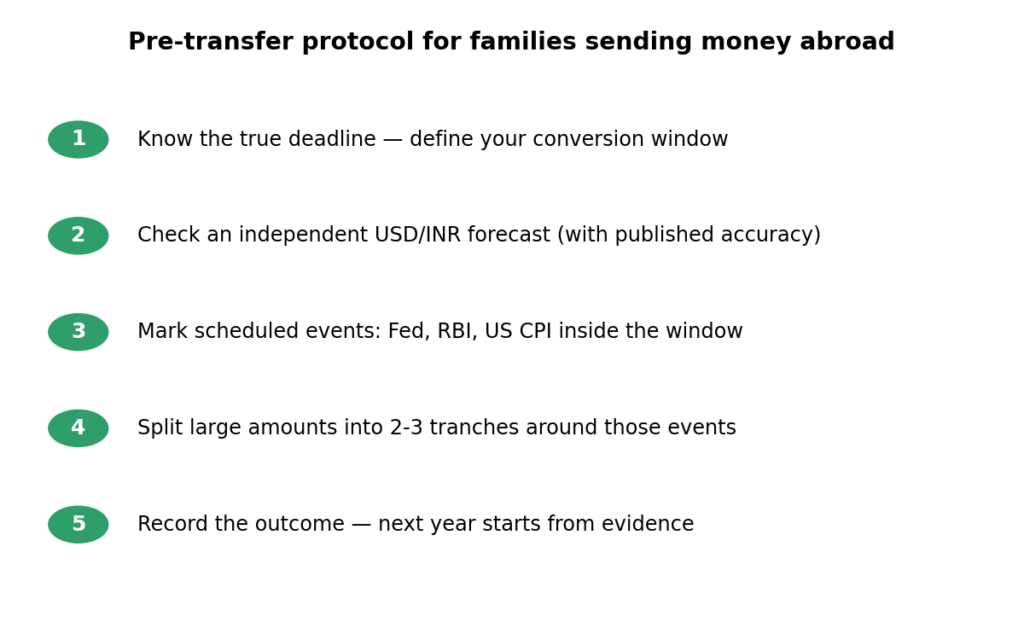

Pre-transfer protocol

A simple protocol any family can follow

Distilled from conversations with financial planners who advise NRI and study-abroad families, the working checklist looks like this: know your true deadline and count backwards to define your window; check an independent forecast with a published accuracy record at the start of that window; mark the scheduled macro events inside it; split large conversions into two or three tranches around those events; and record what you did, so next year’s decision starts from evidence rather than memory.

Each step takes minutes. Together they routinely save more money than most households earn on their savings accounts in a quarter — not by predicting the market, but by refusing to be surprised by it.

This article is for informational purposes only and does not constitute investment or foreign-exchange advice.